On Tax Avoidance and Poverty

On Tax Avoidance and Poverty

A historical perspective on pools of commitments

The term "poor" in the context of lacking money has ancient roots and its evolution in literature is difficult to trace definitively to a single point of origin. The Old English word "pēawer," which eventually became "poor" in Middle English, initially carried connotations of scantiness or meagerness, not necessarily restricted to money but also to possessions or quality of life.

In literature, the use of "poor" to denote a lack of financial wealth appears by the late Middle Ages. For instance, the English poet Geoffrey Chaucer frequently used the term in the 14th century in his works, such as "The Canterbury Tales," to refer to a state of monetary insufficiency among characters.

The shift from broader implications of lack to specifically financial constraints likely paralleled societal changes where monetary wealth became increasingly central to definitions of social status and stability. The precise origin of "poor" in terms of money specifically might be buried deep in historical uses predating these surviving texts, evolving with the language and economic structures of the times.

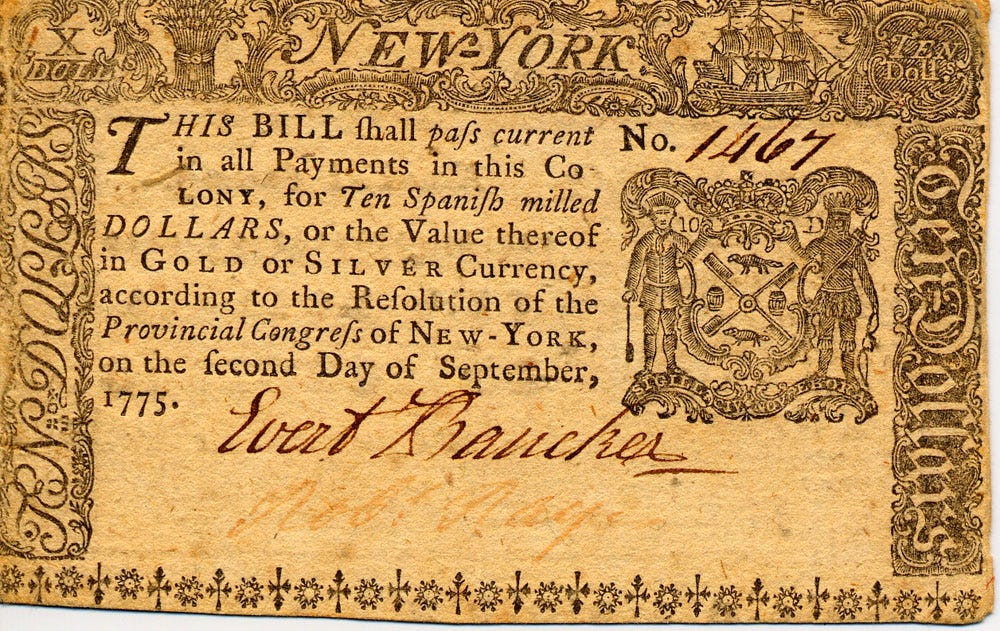

The widespread adoption of the term poverty being association with monetary insufficiency seems to intersect with colonialism and the expansion of empires, such as that of Rome. Both scenarios involved the imposition of new economic systems and social structures, which often included new forms of predatory taxation.

In the context of the Roman Empire, the economic dynamics revolved heavily around taxes, which were typically paid in coinage, reflecting a monetary economy's importance. Those unable to meet tax obligations due to a lack of money (poverty) had severe penalties, including enslavement for debt (wage slavery). The term "proletarius" in Roman society referred to the lowest class of citizens (the proletarii or workers), who owned little or no property and whose primary societal value was considered to be producing offspring and, at times, serving as soldiers. They were named specifically for their economic plight was well recognized in the societal structure.

Parallel to the colonial context, as European powers expanded, they imposed new economic systems upon the peoples they colonized, often including new forms of taxation payable in the colonizers’ currency. This forced integration into a global monetary system frequently disadvantaged indigenous populations, making them "poor" in the colonial economic context. Many indigenous economic systems, which were based on non-monetary forms of exchange, were devalued or disrupted, leading to increased “poverty” under the newly imposed system.

Thus, both in ancient Rome and under colonial rule, the imposition of monetary systems and taxes played significant roles in creating and defining poverty. The terms used to describe those who lacked money were often embedded within larger social and economic frameworks that emphasized the power dynamics between rulers and the ruled.

The perspective of viewing tax avoidance as a form of resistance to parasitic exploitation adds a significant nuance to understanding historical and contemporary economic systems, especially in contexts where the imposition of taxes is, or seen as an extension of colonial or oppressive power structures (We can all name a few countries who’s tax systems have not changed much since colonization).

- Historically, tax systems introduced during colonial times often served the interests of the colonizers more than those of the colonized. They were primarily designed to extract economic value from the colony and transfer it to the colonial power. This form of economic extraction can be seen as parasitic, where the colony serves as a host from which resources are continually drawn without equitable returns. In such contexts, tax avoidance might be viewed not merely as a colonial mandate infringement but as a form of economic resistance or survival tactic by the colonized populations.

- For indigenous and colonized peoples, traditional economies were often self-sustaining and based on reciprocal exchange systems like commitment pooling that did not involve monetary transactions. The introduction of a tax obligation, payable only in the colonizers' currency, forced these populations into the monetary economy, often extremely disadvantageously. Avoiding these taxes could be seen as an attempt to preserve traditional economic practices and resist an externally imposed economic order.

- In modern contexts, tax avoidance is typically framed within legal and ethical debates, often criticized when used by the wealthy or corporations to shirk societal responsibilities. However, when considering communities still recovering from the impacts of historical colonization and economic manipulation, the narrative can shift. Here, tax avoidance might be contextualized as a strategy to retain economic autonomy and safeguard local resources from being disproportionately funneled to a perceived external or unfair governing entity.

This reframing raises important ethical questions about the balance between legal obligations and moral rights, especially in cases where the legal framework is seen as an extension of historical injustices. Let’s challenge conventional views on taxation and its role in society, and have a deeper examination of whom tax systems benefit and at whose expense they operate.

From a grassroots economics perspective, such discussions highlight the need for economic systems and tax policies that are not only legally sound but also equitable and sensitive to the historical and cultural contexts of the populations they serve. This could lead to more inclusive economic models that support sustainable development and rectify historical inequities.

Viewing tax avoidance in this light invites a broader conversation about economic justice, historical accountability, and the paths towards more equitable economic systems. It suggests that understanding the motivations behind avoiding taxes can provide insights into underlying economic disparities and tensions.

Localization: Taxing Commitment Pools

Commitment Pools, as developed in the context of grassroots economic models, can be conceptualized as decentralized systems where participants contribute and exchange resources (goods and services) through formalized commitments, often represented as digital or physical vouchers. These systems are especially pertinent in communities where traditional, non-monetary mutual service practices have been foundational. The essence of such pools is to facilitate local trade and resource sharing without the necessity of national currencies.

Silvio Gesell (one of the most highly acclaimed economists by John Maynard Keynes) proposed the concept of demurrage on currency to discourage hoarding and encourage spending, thereby increasing economic activity. Applying this idea to Commitment Pools, a demurrage fee (or a similar mechanism) is implemented on the formal commitments within the pool. This would mean that the commitments lose value over time unless used, compelling holders to circulate them (and hence issuers to fulfill them) within the community rather than stockpiling. This serves as a form of tax on inactivity or hoarding, encouraging a continual flow of resources and services.

In a system where Commitment Pools use local vouchers as formalized commitments for exchanges, taxing these transactions directly with national currency might not only be impractical but also unjust. Many such local systems operate independently of national infrastructure, deriving their value and functionality from local participation and governance. Therefore, the notion of applying local taxes directly on these transactions in the form of demurrage or similar mechanisms seems more appropriate and sustainable. This kind of tax is inherently local and self-regulating, designed to benefit and sustain the local economy.

The application of taxes within these systems should reflect the nature of the transactions:

1. If taxes are necessary for the maintenance of communal infrastructure or services within the pool’s ecosystem, they should be levied in the same currency as the transactions—i.e., the local vouchers. This ensures that taxes are paid through the same economic activities that benefit from communal resources, without being forced to rely on external monetary systems.

2. Implementing demurrage (gradual expiration and renewal with the issuer) on local vouchers acts as a tax on holding the vouchers without using them, akin to property taxes. This incentivizes active participation and circulation of value within the community, which can be seen as a natural tax and even ancestral system reinforcing communal economic dynamics.

The assumption that all exchanges benefit from national infrastructure and thus should be taxed in national currency requires critical examination. Many local trade systems using Commitment Pools might operate largely independently from national infrastructures, or they might contribute differently to the broader economy. An audit or assessment could determine the actual dependence and impact of local trades on national systems, leading to a more equitable basis for any external taxation.

Back to Libraries

‘Borrowing’ books or toys from a library illustrates how natural constraints on hoarding (limiting the number of books one can borrow at a time and require previous books returned) can regulate the circulation of resources. Similarly, commitment pools can regulate economic behavior by implementing rules that discourage the accumulation of unused vouchers, thus maintaining a dynamic flow of resources and engagements within the community.

Commitment Pools offer a structured yet flexible approach to fostering local economies that can be insulated from the volatility of national currencies and financial systems. By using local vouchers (formal commitments) and imposing holding taxes like demurrage, these pools can sustain active and equitable trade, reflecting the principles of mutual aid and communal resilience. This approach not only challenges traditional economic models but also aligns with sustainable practices that prioritize community well-being over individual accumulation. Note that fees on pool exchanges can be seen as a spatial rather than temporal form of demurrage. As the farther across the network of pools you must go to reach the commitment or assets of your choosing – the larger the cost (hence internalizing an external cost).

Which services?!

The call for specificity in taxation—labeling taxes according to the services they fund—reflects a desire for a more transparent and accountable government. This could involve detailing on receipts or tax bills exactly what taxpayers are funding, such as "Defense Tax" or "Social Security Tax." Such specificity could extend to all aspects of government expenditure:

In example … given that a significant portion of U.S. tax revenue is allocated to military spending, clearly labeling this expenditure as "Defense Tax" on tax statements would make it explicit that these funds are designated for military salaries, benefits, operations, and pensions.

Infrastructure: For services like road maintenance, which benefits from tax dollars but is directly experienced daily by citizens, a "Road Tax" could be applied. This would directly link tax payments to tangible outcomes, such as the construction and repair of roads.

Educational Services: Similarly, taxes for education could be specifically earmarked and shown on tax bills, ensuring that taxpayers can see their contributions to public schooling systems.

Service Taxes and Economic Systems

Embedding transparency within the tax system by clearly labeling where taxes are going helps align taxpayer contributions with visible outcomes, potentially increasing public support for tax policies when they can directly see the benefits. This approach could be formalized through processes like participatory budgeting and community action planning, where community members have a direct say in how public funds are used, enhancing democratic engagement and accountability. As part of a commitment pool or localized economic system, insurance mechanisms can be funded through specific levies or demurrage, providing a safety net for participants and enhancing the stability of the economic system.

Introducing transparency in tax allocation by clearly labeling taxes according to their use can significantly alter public perception and engagement with tax systems. In both national and local contexts, such as in Commitment Pools, this approach not only fosters greater accountability and trust in governance but also aligns tax contributions more closely with community values and needs.

I think it’s really healthy for us to pool our commitments with transparency and clarity while inviting broader rethinking of economic systems, emphasizing participation, and mutual benefit in financial governance.

Please watch:

Hi Will, that's a good summary of the coercive and exploitative nature of national/official/government currencies, and how taxes are an essential element in that process. (Note that the Federal Reserve Act and the Income Tax Act were both passed around the same time). By forcing taxes to be paid using a particular "brand" of money, people are forced to enter the market in which to buy that brand of money, which we do mainly by selling our labor for money. That is one of the greatest obstacles we face in creating the kind of decentralized economies and exchange systems we need. If we are being “paid” in something other than official government money, the government has no legitimate claim on us to pay taxes using official money.

The same situation prevailed in Biblical times. The Temple Tax had to be paid using the Temple Shekel and the money changers in Jerusalem exploited the people in the process of exchanging for it.

The income tax that the IRS collects measures your tax liability in terms of your money income, but money is a claim to real value, not real valuable in itself. Yet, if you are paid “in kind” you have not received any money, but real value. Now the government wants you to somehow get money to pay tax on the “free market value” of the goods or services you received. They want it both ways—tax the claim AND tax the commitment.

One of the most thought provoking articles on economics, money, and taxes I have read in a very long time. Thanks Will!